Summary

Modern financial infrastructure is replacing slow, costly cross-border payment systems with faster, more transparent rails. By giving businesses direct access to wholesale liquidity, multi-network settlement, and cross-asset liquidity across fiat and stablecoins, new platforms reduce intermediaries, free trapped capital, and enable global money movement in minutes instead of days.

Nostro/Vostro

Capital Efficiency

Payment Routing

The Ledger Gap

Money moves globally, but no global ledger exists. Each country runs its own monetary system with an independent ledger, so the world bridges ledgers with correspondent banks and pre-funded capital sitting in nostro-vostro accounts. Every cross-jurisdictional flow (payments, investment, trade, lending) runs through this bridge.

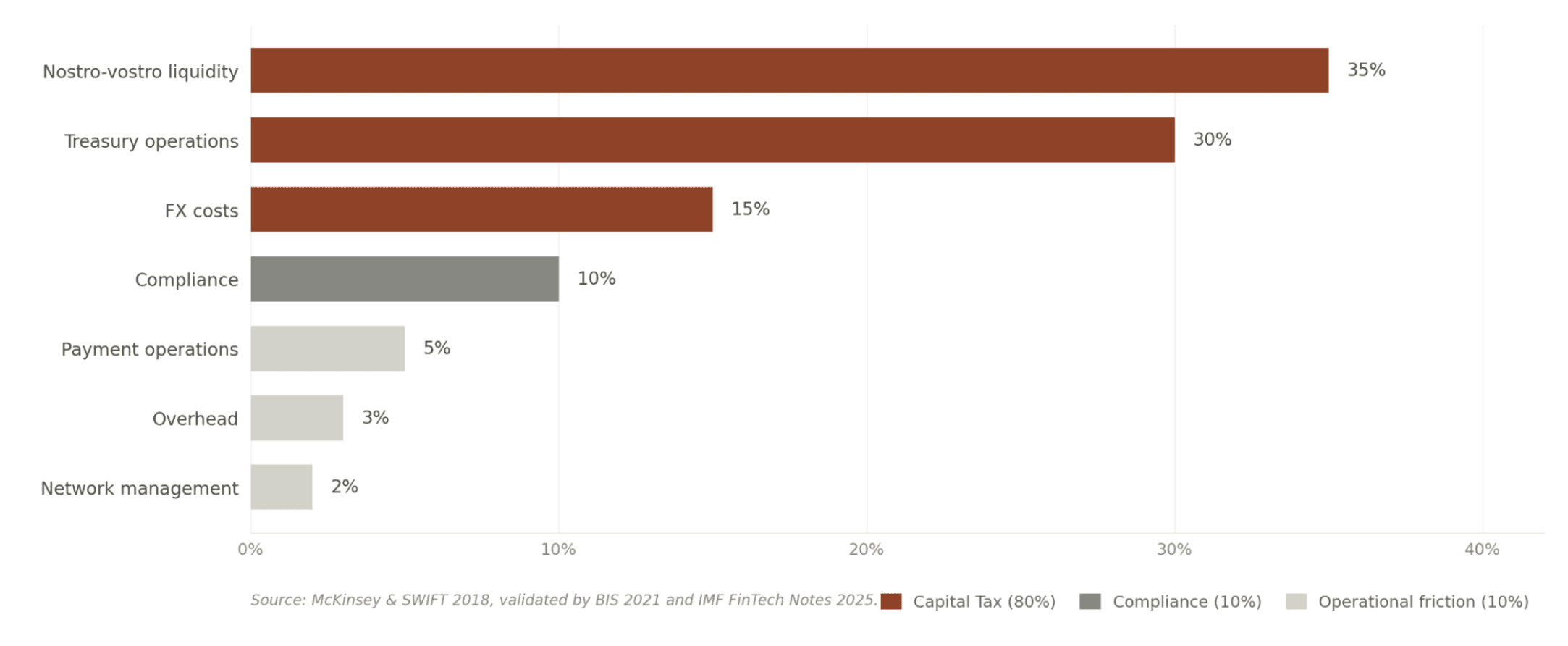

The Capital Tax

Bridging the Ledger Gap is expensive, and the cost has three faces:

The carry cost: pre-funded capital sitting idle to make flow possible. ~35% of the cost stack. ~$4 trillion trapped globally in nostro-vostro accounts (BIS estimate; broader industry estimates run as high as $27 trillion).

The treasury management cost: the operational machinery required to keep the system functioning. Intraday liquidity forecasting, reconciliation across hundreds of correspondent relationships, balance sheet FX hedging, buffer sizing. ~30% of the cost stack.

The currency exchange cost: FX spreads charged at every conversion point along the chain. ~15% of the cost stack.

The largest cost in the global money movement stack is not the wire fees, not the compliance overhead, not the network charges. It's the carrying cost of trapped capital, the cost of managing that capital, and the spreads charged to exchange it. Together 80% of the all-in cost.

Compliance is 10%. Everything else (payment operations, network management, overhead) is below 10% combined.

Exhibit A - The cost stack of global money movement

Blockchain is necessary but not sufficient

While blockchains act as global ledgers and work great for single-asset transfers where no currency conversion is required, the Capital Tax re-emerges in multi-currency transactions. For example, if a user pays in USDC and the recipient requires MXN, a liquidity provider must hold that asset to lock in the price, re-inserting the trapped capital inefficiency.

Programmatic attempts like Automated Market Makers (AMMs) are structurally inefficient for institutional FX. They rely on locked liquidity in pools, and at global scale, the capital required to avoid slippage would effectively recreate the nostro-vostro problem on a different ledger.

Blockchains have made progress on the 80%; faster settlement reduces dwell time, programmable rails compress treasury overhead. But the structural requirement is unchanged: someone still has to hold inventory to enable the exchange. Stablecoins reduce the carrying cost of that inventory but they do not eliminate the need for it. The 80% is the work that remains.

What eliminating the Capital Tax requires

The Capital Tax is an architectural problem. Faster rails built on top of pre-funded capital reduce friction at the edges but leave the structural cost intact. Eliminating the Capital Tax requires settlement infrastructure architected around capital velocity (how much flow each dollar of capital supports per unit of time) not around the speed of the rails it travels on.

Any architecture that genuinely eliminates the Capital Tax has to satisfy two conditions simultaneously.

The first is smart routing: finding the optimal execution path for every transaction in real time across a fragmented liquidity landscape. This means selecting the right venue, sequencing, and sizing for each flow to minimize the cost of conversion at the moment it occurs.

The second is smart capital allocation: treating capital itself as a fleet to be dynamically deployed, not pre-positioned inventory to be held. Capital moves across currencies, rails, and counterparties in response to real-time demand, minimizing the idle capital that constitutes the carry cost.

These two conditions are not independent. Routing without dynamic capital allocation still requires pre-funding at each node. Capital allocation without optimal routing has no signal; it cannot know where to deploy capital, when, or at what cost.

A useful analogy is Uber. Uber optimizes two things simultaneously: passenger wait time and driver utilization. Minimizing wait time is the routing problem: get the nearest available car to the passenger as fast as possible. Maximizing utilization is the capital problem: keep each car earning, not sitting idle. The insight is that these objectives are not in tension; solving both together is precisely what makes the network valuable. The same logic applies here. Transactions need to clear as close to real time as possible. Capital needs to be deployed, not parked. An architecture that optimizes only one leaves most of the value on the table.

The Capital Tax collapses only when both conditions operate together and only when they operate at scale. The reason scale matters is mathematical.

Why the right architecture gets better with scale

The capital required to support a flow depends on one variable above all others: how long each dollar spends in the system. The relationship is precise: the working capital deployed equals the rate of flow multiplied by the average time each dollar dwells in the system.

Put simply, cut dwell time in half and the same dollar of capital supports twice the volume. This is why settlement speed matters structurally, not just operationally.

In a conventional system, scaling volume scales capital requirements proportionally. Double the throughput, double the pre-funded capital. The cost structure is linear.

In a networked settlement system, one where flows increasingly offset each other internally, the relationship breaks from linear. Working capital grows more slowly than the flow it supports.

The consequence is that each additional dollar of throughput demands progressively less incremental capital to support it. The cost of liquidity falls as the network thickens. The system gets cheaper to operate per unit of flow precisely because it is handling more flow.

Returning to the Uber analogy: this is what happens to a ride-sharing network as it densifies. More drivers mean shorter wait times, which means more rides per driver per hour, which means the network can serve more passengers with proportionally fewer cars. The efficiency compounds. The same dynamic applies to settlement infrastructure: more flow means more internalization, more internalization means less idle capital, less idle capital means lower cost per unit of flow.

This is not a network effect in the loose sense the term is usually used. It is a mathematically precise compounding relationship.

The market structure

Global money movement organizes into three structural layers:

Issuance: stablecoins, tokenized treasuries, tokenized RWAs. The asset layer.

Settlement infrastructure: the layer where capital is made productive across the Ledger Gap. Where flows clear, capital is allocated, and the Capital Tax is either paid or eliminated.

Distribution: exchanges, fintechs, payments companies. The customer relationship layer.

Blockchains are settlement primitives that the settlement infrastructure layer composes. Use cases compose across all three layers: payments, lending, investments. Each requires an asset, a settlement layer, and a distribution channel. Companies can operate across multiple layers, but the layers themselves are distinct, and capital efficiency lives in the settlement layer.

The settlement infrastructure layer is use-case independent. The engine doesn't care whether the flow is FX, credit deployment, treasury rebalancing, or settlement of a tokenized security. It cares about dwell time, capital allocation, and routing efficiency. As use cases proliferate, the same substrate carries more flow, compounding the flywheel.

The long arc

The question isn't what will change but what won't. Money will always need to move faster, with less friction, and with less idle time. As long as people convert between distinct assets and that conversion takes any time at all, the Capital Tax will exist. And as on-chain finance multiplies the number of distinct assets (currencies, tokenized treasuries, tokenized stocks, tokenized RWAs) the surface grows.

The architecture that drives the Capital Tax toward its physical limit will define the next era of global finance.

Ready to unlock capital efficient money movement?

Infrastructure for capital-efficient FX. Moving money at the speed of information.

System status · OperationaL

v 2026.5